Factors That Affect Car Insurance Premium in UAE

- ١٨ مايو ٢٠٢٦ م

The prices of car insurance in the UAE are not accidental. Two motorists with different vehicles may pay different sums to cover, since insurance firms assess risk differently for each car-driver mix. This is why people are frequently lost in the comparison of policies and the significant price difference.

The truth is that there are a number of aspects that affect your Car Insurance Premium. Insurance rates can be influenced by your age, driving history, car model, claim history, location, and even the way the vehicle is maintained. There are certain factors that are risk-aggravating to insurers and others that are beneficial in driving down premium costs.

Knowledge of these aspects of car insurance in UAE helps motorists make more informed decisions before buying or renewing their insurance policies.

What Is a Car Insurance Premium?

"Car Insurance Premium in UAE refers to the sum that is paid to an insurance firm to cover the protection of the vehicle. The premium is determined by the insurer's assessment of the likelihood that the driver or the vehicle will experience accidents, theft, damage, or subsequent claims.

An increased perceived risk typically implies the following:

- Higher premium cost

- More coverage restrictions

- Higher claim sensitivity

Lower perceived risk usually creates the following:

- Better pricing

- Easier approval

- More stable renewal costs

Why Car Insurance Premiums Differ Between Drivers

Premiums are not calculated using the same formula across insurance companies. All policies are based on risk assessment, and risk varies by driver.

- Driver Risk Profile Changes Pricing: Insurance companies consider age, experience and driving history to determine the likelihood of future claims.

- Vehicle Type Affects Insurance Risk: Luxury, sports, and high-value cars tend to increase car insurance cost UAE, as their repair and replacement costs are higher.

- Claim History Influences Premium: Drivers with repeated claims are often considered higher risk during policy renewal calculations.

- Usage Pattern Matters: Commuter cars tend to have higher premium rates than low-usage cars.

Crucial Factors Affecting Car Insurance UAE

Most drivers believe that insurance prices are based only on the car model or the type of cover. However, in practice, risk is calculated by insurance companies with a combination of factors.

Insurance companies in UAE consider how you drive, your car condition, your claim history and even your place of driving as the factors that determine your Car Insurance Premium. These factors will be understood to help drivers make wiser financial and ownership decisions for their vehicles.

- Driver Age and Experience

The younger or less experienced drivers are usually considered riskier by insurance companies because they have a higher chance of accidents than older, more experienced drivers. Drivers with clean, longer driving records tend to be charged a higher premium and receive more favourable renewal terms in the long run.

- Vehicle Type and Market Value

The luxury cars, sports cars, and high-end SUVs tend to drive up the price of car insurance in UAE due to the high cost of repair, spare parts, and replacement costs are much higher than those of ordinary cars.

- Previous Claim History

The number of accidents or insurance claims is also likely to raise the prospective premiums. Drivers with a claim-free history are typically offered better rates because insurers consider them low-risk policyholders.

- Coverage Type Selection

Extensive insurance is, of course, more expensive than third-party insurance because it offers broader coverage for accidents, theft, fire, and other damage-related incidents. The amount of coverage directly impacts the premium.

- Daily Driving and Vehicle Usage

Vehicles that are highly commuted or driven over long distances have a higher exposure on the road, and they are prone to accidents. Increased usage will normally translate into increased insurance risk calculations.

- Traffic Violations and Driving Behavior

Fines, speeding, or risky driving history is repetitive, which adversely affects the insurer's confidence. Insurers tend to charge more to drivers with a bad driving history.

- Location and Parking Conditions

Cars used on a daily basis and parked in open, high-prone conditions in urban centres might be charged a higher premium, as the risk of accidents and damage is serious.

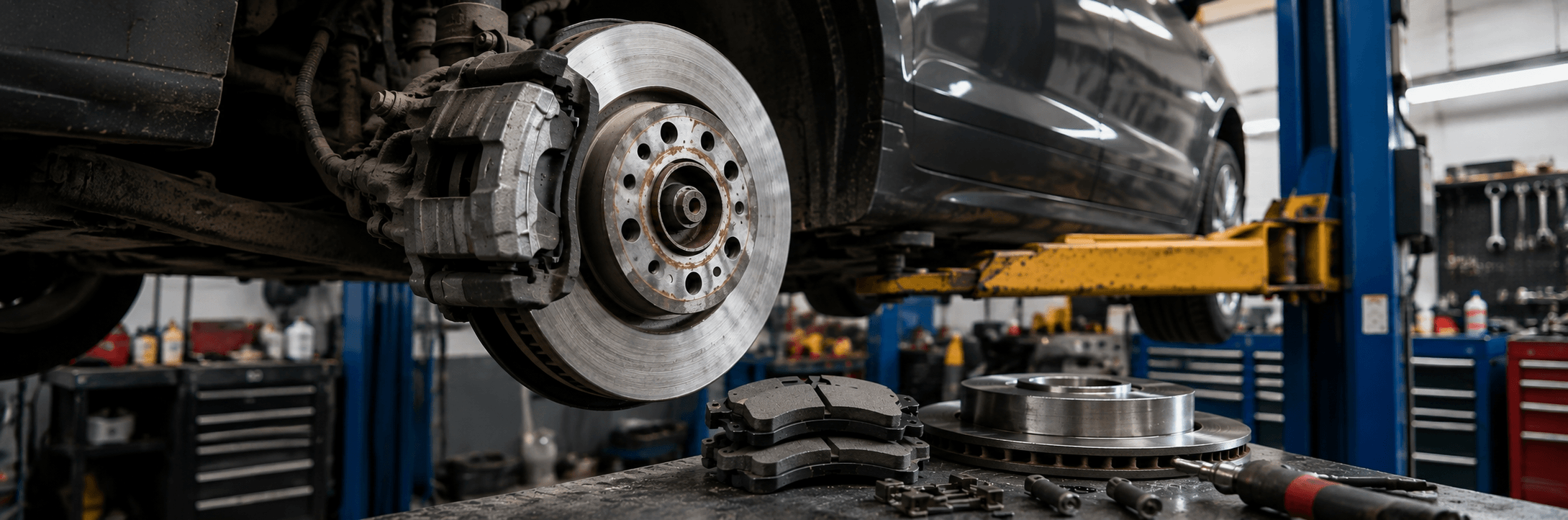

- Vehicle Maintenance and Condition

Properly maintained vehicles tend to be safer and have a lower risk of mechanical failures at any time. Indirect impact on insurance risk perception in the future may be caused by poor tyre condition, brake issues, or lack of maintenance.

- Repair and Spare Part Cost

Cars requiring imported or expensive spare parts often have higher insurance premiums because claim settlement costs are higher for insurers.

- No-Claim Bonus Eligibility

Drivers who avoid making claims over long periods often qualify for no-claim benefits, helping reduce long-term car insurance price factors UAE significantly at policy renewal.

Comprehensive vs Third-Party Insurance

The type of insurance coverage selected directly changes the premium amount because the coverage scope differs significantly.

Comprehensive policies usually cost more because they protect against a broader range of damage scenarios.

Common Mistakes That Increase Insurance Premium

Many drivers unknowingly increase their insurance cost through avoidable habits and decisions.

- Delaying Insurance Renewal: Policy gaps sometimes negatively affect renewal pricing.

- Ignoring Driving Violations: Repeated traffic fines and violations increase insurers' perceived risk.

- Choosing Coverage Without Comparison: Not comparing policies often leads to unnecessarily higher premium payments.

- Neglecting Vehicle Condition: Poor vehicle maintenance may increase the risk of accidents or breakdowns over time.

How Vehicle Maintenance Impacts Insurance Risk

Most drivers do not see the relation between vehicle maintenance and insurance, yet they are closely related. Insurance companies define risk in terms of the probability of accidents, breakdowns and claims. Such a vehicle is more likely to pose a risk due to the direct impact of mechanical faults on driving safety, braking, and road stability.

This is why the behaviour of Car Insurance Premiums in the long run is affected indirectly by regular maintenance.

- Tyre Condition Affects Road Safety

Worn tyres reduce grip, braking performance, and vehicle stability, particularly when the driver has to apply emergency braking or when the vehicle is on wet roads. Tyre condition is a risk factor that increases the likelihood of accidents, leading to long-term insurance exposure.

- Brake Performance Reduces Accident Risk

Lack of strong brakes, slow reaction to stopping, or unmaintained brakes make collisions very dangerous. Proper brake maintenance enhances car safety and minimises the possibility of car accident insurance claims.

- Engine Reliability Prevents Roadside Failures

Lack of proper engine maintenance puts the risk of breakdowns, overheating or abrupt vehicle failure on the road. Stable engine status facilitates safer road operation and reduces risk of operations.

- Battery and Electrical Health Improve Reliability

Sudden breakdowns or other safety-related malfunctions may occur due to weak batteries or unstable electrical systems. Regular maintenance minimizes sudden vehicle breakdowns.

- Suspension and Alignment Affect Vehicle Control

Damaged suspension or poor wheel alignment affects steering stability, tyre wear, and overall road handling. Better vehicle control reduces the probability of accidents during daily driving.

- Regular Servicing Reflects Responsible Ownership

Drivers who maintain their vehicles regularly are often viewed as lower-risk vehicle owners because proper maintenance reduces preventable mechanical issues and unsafe driving conditions.

- Lower Mechanical Failure Means Lower Claim Risk

Well-maintained vehicles are less likely to experience mechanical failures that contribute to accidents or roadside emergencies. Reduced claim probability indirectly supports better insurance stability over time.

Conclusion

Being aware of the key drivers of car insurance UAE allows drivers to make more financially sound and car ownership choices. The cost of insurance is affected by so much more than the car itself: driving history, car type, claim history, usage and maintenance all come into play in determining your Car Insurance Premium in UAE.

The drivers with safer driving habits and well-maintained vehicles usually lower the risk of ownership and insurance costs in the long term. And as insurance is effective in case of unforeseen circumstances, taking good care of the vehicle will minimize these risks in the first place.

TyresCart assists UAE drivers in replacing their tyres, aligning them, and replacing the battery, and offers vehicle maintenance solutions to keep their vehicles safe, reliable, and performing optimally on the road daily.